Long-term care is costly, and most physicians underestimate future needs.

Traditional LTC insurance offers more flexibility, but it’s “use it or lose it.”

Hybrid LTC insurance combines care with life insurance or annuities—no wasted premiums.

Hybrid policies cost more upfront but give a guaranteed benefit, even if care isn’t needed.

Choosing the right LTC plan now protects your retirement and legacy.

As a physician or dentist, you spend your career taking care of others, but have you thought about who will take care of you when you’re older?

Long-term care (LTC) is expensive, and many people underestimate how much help they might need later in life. Whether it’s home care, assisted living, or a nursing facility, the costs can drain even a strong retirement plan.

That’s where long-term care insurance comes in. But not all policies are the same. There are two primary types:

Traditional Long-Term Care Insurance

Hybrid Long-Term Care Insurance (Life + LTC or Annuity + LTC)

Each has pros and cons, and choosing the right one depends on your financial goals. Let’s break them down.

Traditional Long-Term Care Insurance

What It Is

Traditional long-term care insurance is a standalone policy designed only for long-term care expenses. You pay annual premiums, and if you need care later in life, the policy covers your costs up to a set benefit limit.

How It Works

You choose how much coverage you want (daily or monthly benefit amount).

You select a benefit period (how long benefits will last, such as 3, 5, or 10 years).

There is typically a waiting period (e.g., 90 days) before benefits begin.

If you never need care, you get nothing back—just like auto or health insurance.

Pros of Traditional LTC Insurance

✅ Lower Premiums Initially – Monthly or annual premiums are often lower than hybrid policies.

✅ Comprehensive Coverage – Covers home care, assisted living, and nursing facilities.

✅ Greater Flexibility – Can be customized with inflation protection and shared care for couples.

✅ Potential Tax Benefits – Premiums may be tax-deductible (especially for business owners).

Cons of Traditional LTC Insurance

❌ “Use It or Lose It” – If you never need long-term care, the money you paid in premiums is lost.

❌ Premiums Can Increase – Insurance companies have the right to raise rates over time.

❌ Stricter Underwriting – You may not qualify if you have pre-existing health issues.

Who Should Consider It?

You want the most affordable long-term care coverage.

You’re okay with the risk of not using it (like auto insurance).

You don’t need life insurance or an annuity.

Hybrid Long-Term Care Insurance (Life + LTC or Annuity + LTC)

What It Is

Hybrid policies combine long-term care benefits with either life insurance or an annuity. This way, even if you never need long-term care, your money isn’t wasted.

Types of Hybrid LTC Policies

Life Insurance with a Long-Term Care Rider

A permanent life insurance policy (like whole life or universal life).

If you need LTC, you can use part of the death benefit early to pay for care.

If you don’t need LTC, your beneficiaries receive the full death benefit.

Annuity with Long-Term Care Benefits

You invest a lump sum into an annuity that grows tax-deferred.

If you need LTC, the annuity pays out much more than the original investment.

If you never need care, you or your heirs still receive the annuity funds.

Pros of Hybrid LTC Insurance

✅ “Use It or Keep It” – If you don’t need LTC, your heirs get a death benefit or annuity payout.

✅ Fixed Premiums – Most hybrid policies are paid upfront or have guaranteed level premiums.

✅ Easier to Qualify – Some hybrid policies have simpler underwriting than traditional LTC.

✅ Cash Value Growth – Whole life policies with LTC riders accumulate cash value.

Cons of Hybrid LTC Insurance

❌ Higher Cost – Hybrid policies often require a larger upfront investment.

❌ Less Flexibility – The LTC benefit is tied to the life insurance or annuity, limiting options.

❌ Lower LTC Benefits – Compared to a standalone LTC policy, a hybrid policy may provide less coverage.

Who Should Consider It?

You want LTC coverage but don’t want to waste money if you don’t use it.

You already need life insurance and want to add an LTC benefit.

You have a large amount of cash and prefer to fund an annuity-based plan upfront.

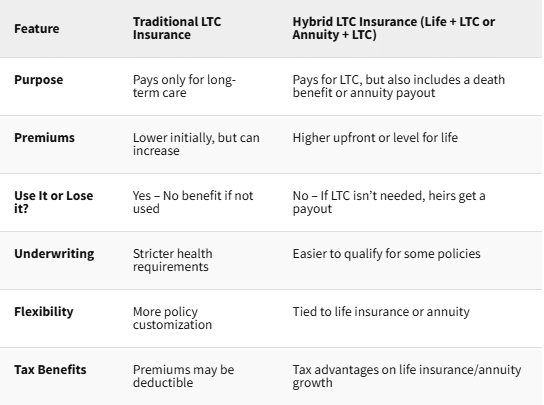

Key Differences: Traditional vs. Hybrid LTC

Feature

Traditional LTC Insurance

Hybrid LTC Insurance (Life + LTC or Annuity + LTC)

Purpose

Pays only for long-term care

Pays for LTC, but also includes a death benefit or annuity payout

Premiums

Lower initially, but can increase

Higher upfront or level for life

Use It or Lose it?

Yes – No benefit if not used

No – If LTC isn’t needed, heirs get a payout

Underwriting

Stricter health requirements

Easier to qualify for some policies

Flexibility

More policy customization

Tied to life insurance or annuity

Tax Benefits

Premiums may be deductible

Tax advantages on life insurance/annuity growth

Which Type of LTC Insurance Is Right for You?

💡 Choose Traditional LTC Insurance if:

✔️ You want the lowest cost LTC coverage.

✔️ You’re okay with the risk of not using it.

✔️ You prefer customizable benefits (e.g., inflation protection, shared care).

💡 Choose Hybrid LTC Insurance if:

✔️ You want LTC coverage + a life insurance benefit.

✔️ You already need permanent life insurance.

✔️ You prefer guaranteed premiums (no risk of future rate increases).

✔️ You have cash to invest upfront for an annuity-based plan.

Final Thoughts

Long-term care can be one of the biggest expenses in retirement. The key is planning ahead so that you’re not caught off guard.

👉 Step 1: Decide how you want to pay for long-term care—self-funding, insurance, or a mix.

👉 Step 3: Work with a financial advisor who understands physician and dentist finances.

The right long-term care plan protects your assets, your independence, and your family’s financial future. Whether you choose traditional or hybrid, making a plan today will give you peace of mind for tomorrow.

Ready to protect your future?

Get a personalized side-by-side policy comparison of the leading disability insurance companies from an independent insurance broker.